.png)

The Beijing summit yielded rose seeds for the White House garden, but for Taiwan, the silence was deafening. Just three days prior (May 8, 2026), Taiwan’s legislature finally authorized a $25 billion self-funded arms budget to procure U.S. hardware, including critical HIMARS systems. This move was a strategic attempt by Taipei to fulfill President Trump’s 'pay-to-play' defense expectations and lock in American support before the Trump-Xi summit could result in a new regional 'grand bargain'."

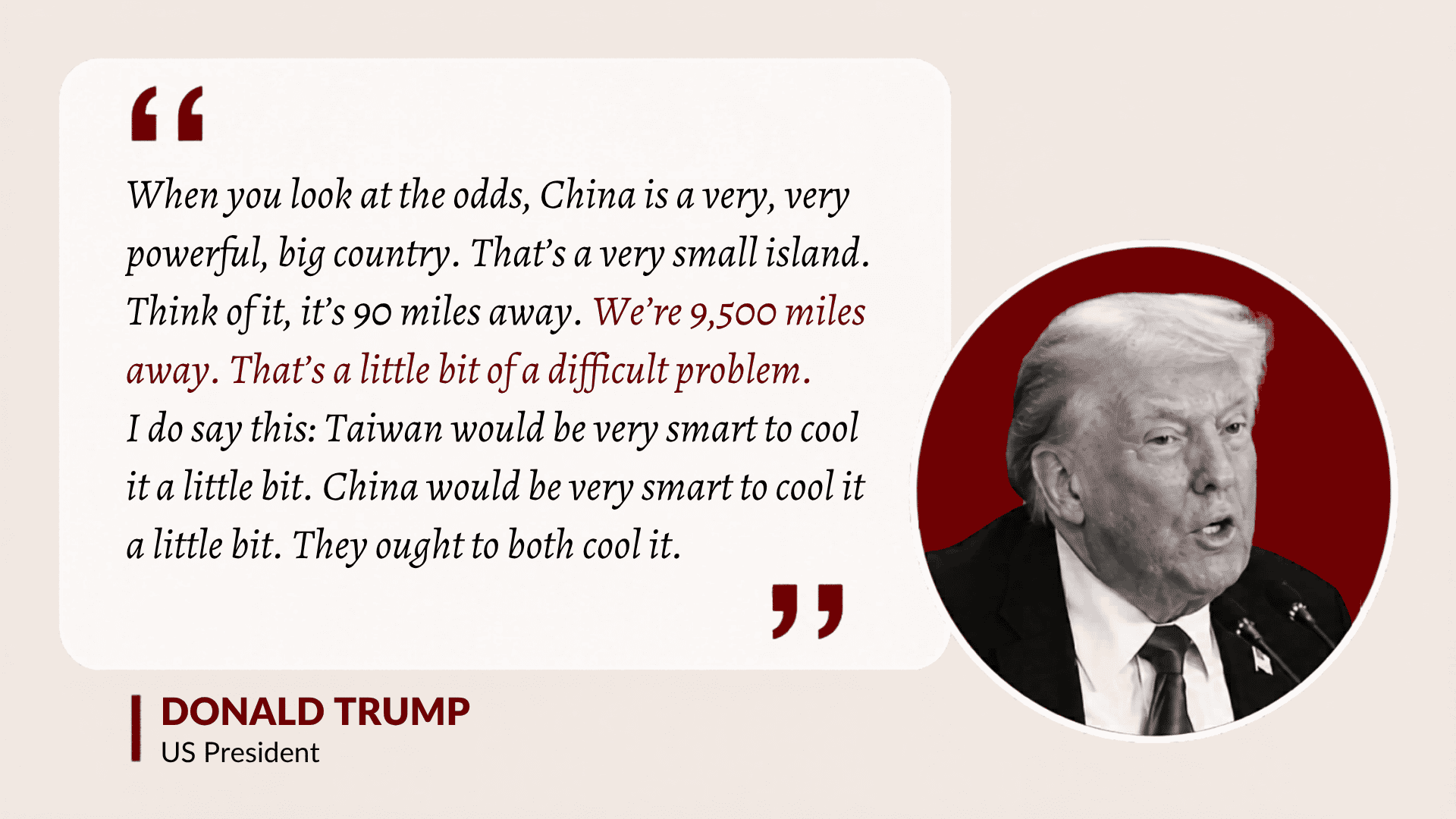

However, President Trump’s rhetoric has shifted toward "transactional uncertainty." His warnings for Taiwan to "cool down" and his reluctance to commit 9,500 miles away while the U.S. remains occupied in Iran and Ukraine have shattered the illusion of a guaranteed shield.

The Transmission to Capital Flows: This perceived shift in the regional security architecture has catalyzed a strategic reallocation of private wealth. In this environment, capital is increasingly seeking stability in jurisdictions perceived as safe havens, with Japan emerging as a primary destination for wealth preservation.

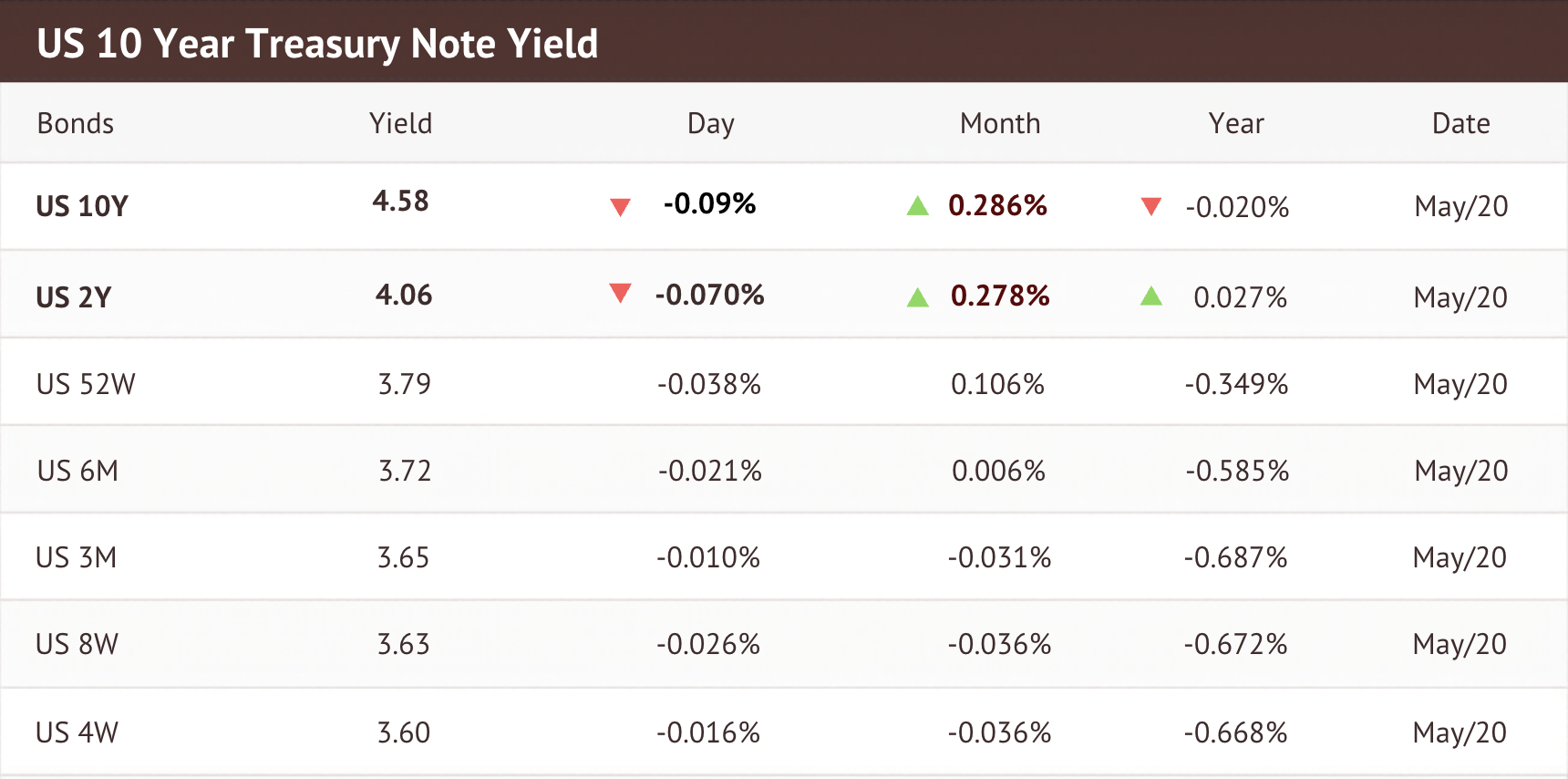

In New York, the bond market is facing a “Bear Steepener”, a technical term for when long-term interest rates rise much faster than short-term ones, typically occurs when the market begins to price in higher inflation expectations or fiscal concerns rather than immediate central bank action. The 2Y Treasury remains anchored at 4.05%, but the 10Y yield has surged to 4.59%. This makes the yield curve steeper and borrowing costs for mortgages and corporate loans more expensive, creating a painful normalization for the broader economy and directly linked to the Bank of Japan’s (BOJ) strategic signaling.

The Internal Pressure: Following the April meeting, internal BOJ voting dynamics reveal growing pressure for a June hike. However, Governor Ueda is strategically prolonging the action to maintain "calculated uncertainty." The goal is to support JPY stability without triggering a panic, but this delay forces a dangerous secondary effect: forced selling of Treasuries.

• The Bessent Factor: U.S. Treasury Secretary Scott Bessent has been vocal in his support for a BOJ hike. Why? Because Japan must sell U.S. Treasuries to provide the dollar liquidity needed to defend a weak yen.

• The Catch: If the BOJ hikes too aggressively to satisfy Washington, it risks a disorderly collapse of the global carry trade, spiking global borrowing costs and potentially forcing a "cut to zero" financial crisis response.

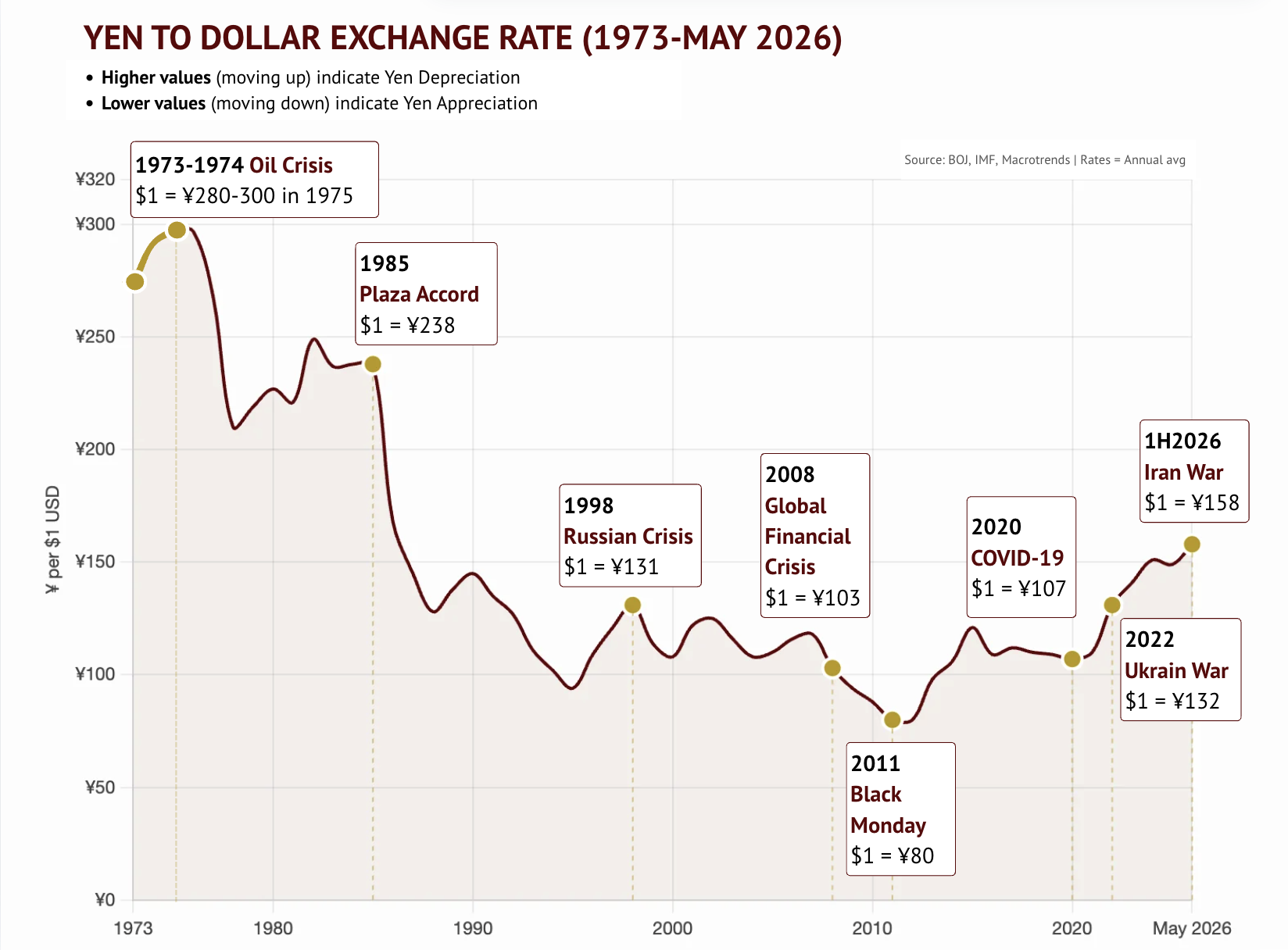

For years, the USD/JPY carry trade functioned as the "infinite money glitch" of global finance, fueled by the vast interest rate differential between the FED and the BOJ. However, as of May 2026, this structural integrity is failing as rate convergence begins. Historical data confirms that this transition frequently leads to a "Snapback Scenario"—a violent, reflexive appreciation of the Yen triggered by global deleveraging.

Every major systemic shock over the last 50 years has resulted in a significant surge in Yen value. Following the 1973-1974 Oil Crisis, the Yen strengthened from its ¥280–300 range down to ¥176 by 1978, during the 1998 Russian Crisis, the Yen snapped back to ¥131; during the 2008 Global Financial Crisis, it surged to ¥103; and in the 2020 COVID-19 pandemic, it strengthened to ¥107. The most extreme example remains the 2011 “Black Monday" era, where the Yen reached a record high of ¥80.

The mechanism is a self-reinforcing spiral. A global shock or U.S. credit event forces immediate risk reduction, requiring traders to liquidate dollar-denominated assets to buy back the Yen they originally borrowed at near-zero rates. This initial buying pressure strengthens the Yen, which in turn triggers cascading margin calls on remaining carry positions. This forces a disorderly unwind that intensifies Yen demand and spikes global volatility, proving that in times of crisis, the Yen does not just stabilize—it aggressively recaptures value.

SOURCES:

- [CNBC] Trump says China and Taiwan should ‘both cool it’, on May 15,2026

- [LIANHEZAOBAO] Survey: Taiwanese buyers of Japanese real estate surge, accounting for 60% of foreign buyers (in Mandarin), on May 10, 2026

- [Reuters] BOJ locks in June rate hike in a risky bet that nothing gets worse, on April 30, 2026

- [The JapanTimes] BOJ signals possible June rate hike amid inflation risks from Mideast war, on May 12, 2026

- [Reuters] US,Japan agree excess FX volatility undesirable, Bessent says, on May 12,2026

- [ANI] "Fundamentals of Japanese economy strong and resilient": Bessent praises Japan's economic resilience during Tokyo visit, on May 13,2026

- [Bank of England] The yen/dollar exchange rate in 1998: views from options markets, Quarterly Bulletin 1991 Q1

-min.jpg)