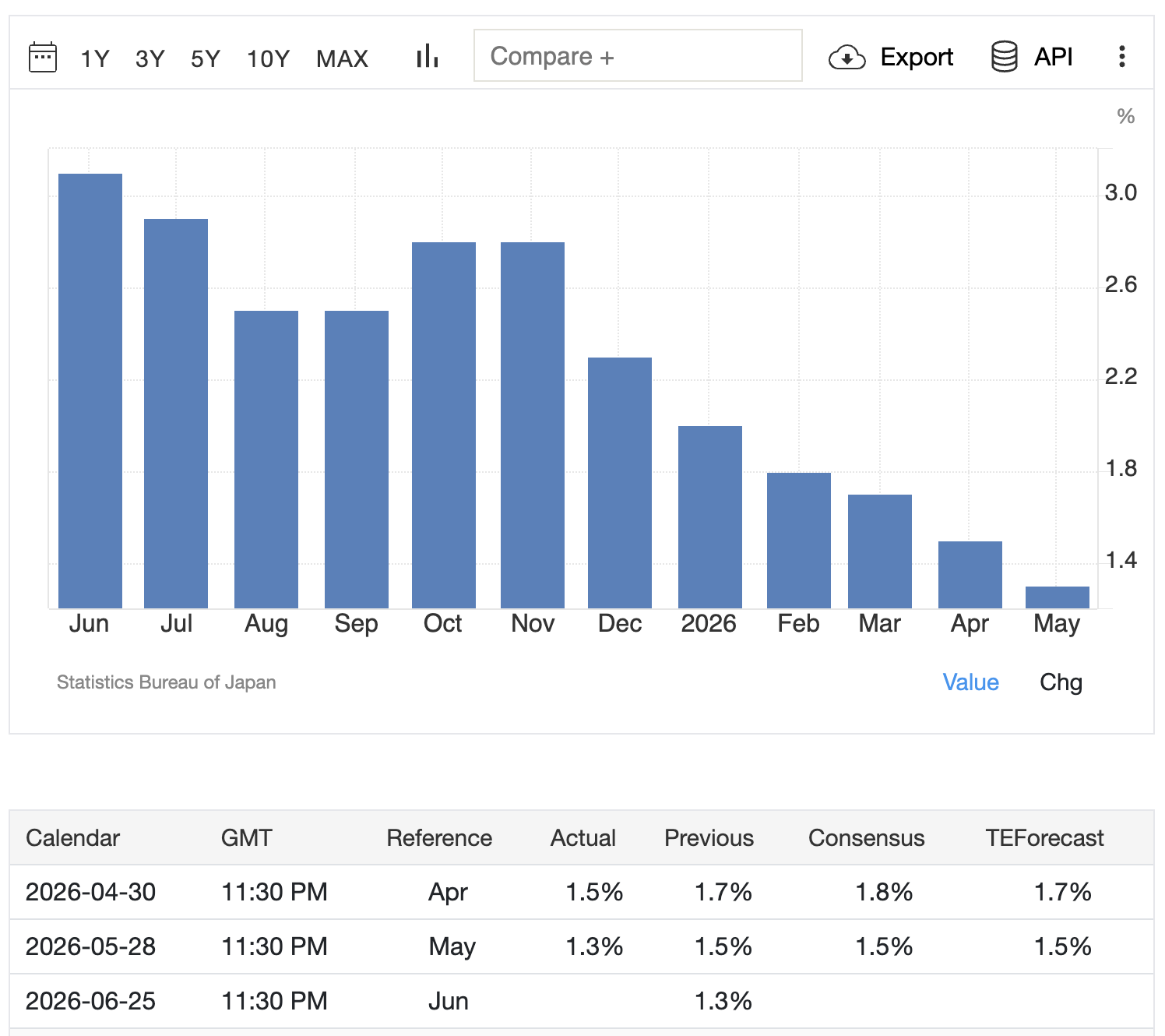

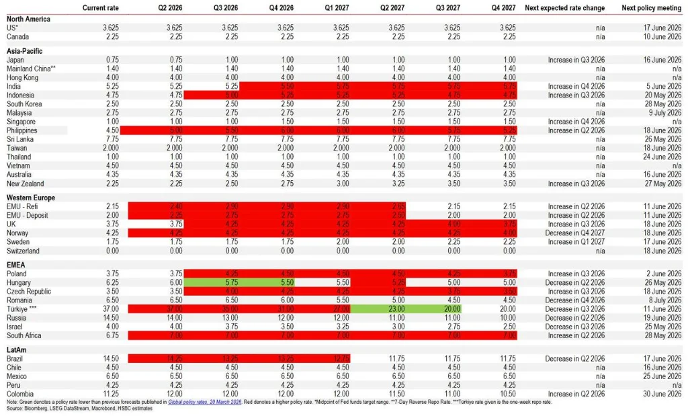

The Bank of Japan is currently trapped between economic data and political optics. Tokyo’s core CPI rose just 1.3% year-over-year in May, missing the 1.5% forecast and remaining well below the BOJ’s 2% target. Typically, this would signal a pause. However, the BOJ’s internal power map reveals a different imperative.

Governor Kazuo Ueda chairs a 9-member Policy Board that is deeply fractured. As of late May 2026, the board is split into three distinct camps:

• Hawks (3 votes): Takata, Tamura, and Nakagawa. All three voted to raise rates to 1.0% in April, prioritizing inflation sustainability over growth concerns.

• Doves (4 votes): Governor Ueda, Deputy Governors Uchida and Himino, and External Member Asada. They favor gradualism, citing weak real wage growth and fragile consumer sentiment.

• Swing Votes (2 votes): Masu and Koeda. These two members hold the deciding power.

The critical insight is temporal. The current “Hawk” influence is peaking in Q2-Q3 2026. Key hawkish members’ terms expire in 2027, and Prime Minister Sanae Takaichi’s administration is poised to appoint more reflationist allies to the board by 2028. This creates a “use it or lose it” window for tightening. If the BOJ does not hike in June, it may lose the voting majority to do so for the next two years. Consequently, despite soft Tokyo CPI, the path of least resistance for the BOJ is a tactical hike to secure policy normalization before the political tide turns dovish.

Market pricing reflects this uncertainty. MNI reports that senior BOJ officials continue to debate the merits of a June hike, with Governor Ueda’s recent speeches serving as key signaling mechanisms ahead of the June 16-17 meeting.

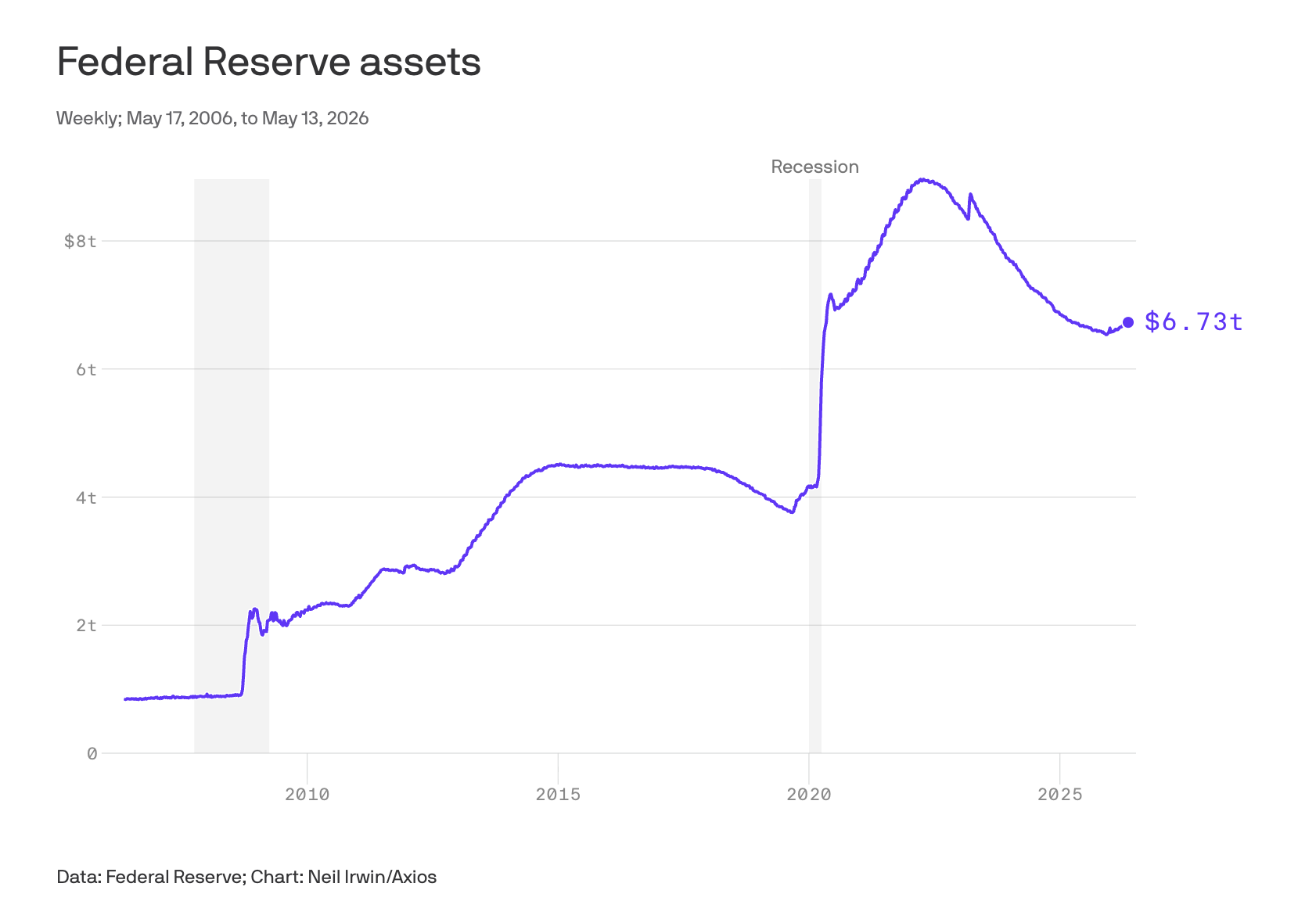

In the US, the transmission mechanism has shifted from the Federal Funds Rate to the Balance Sheet. With the Fed Funds target range holding at 3.50%-3.75% since early 2026, Chair Kevin Warsh has abandoned traditional rate hikes as his primary tool. Instead, he is aggressively pursuing Quantitative Tightening (QT) to shrink the $6.7 trillion balance sheet.

Warsh’s strategy is twofold:

Redefining Inflation: Warsh has argued for shifting the Fed’s preferred inflation gauge from Core PCE to Trimmed Mean PCE. By excluding extreme tail-risk price shocks, Trimmed Mean PCE currently reads lower (~2.3-2.8%) than Core PCE (3.3%). This allows Warsh to claim inflation is "under control" without cutting rates, providing political cover for tighter financial conditions.

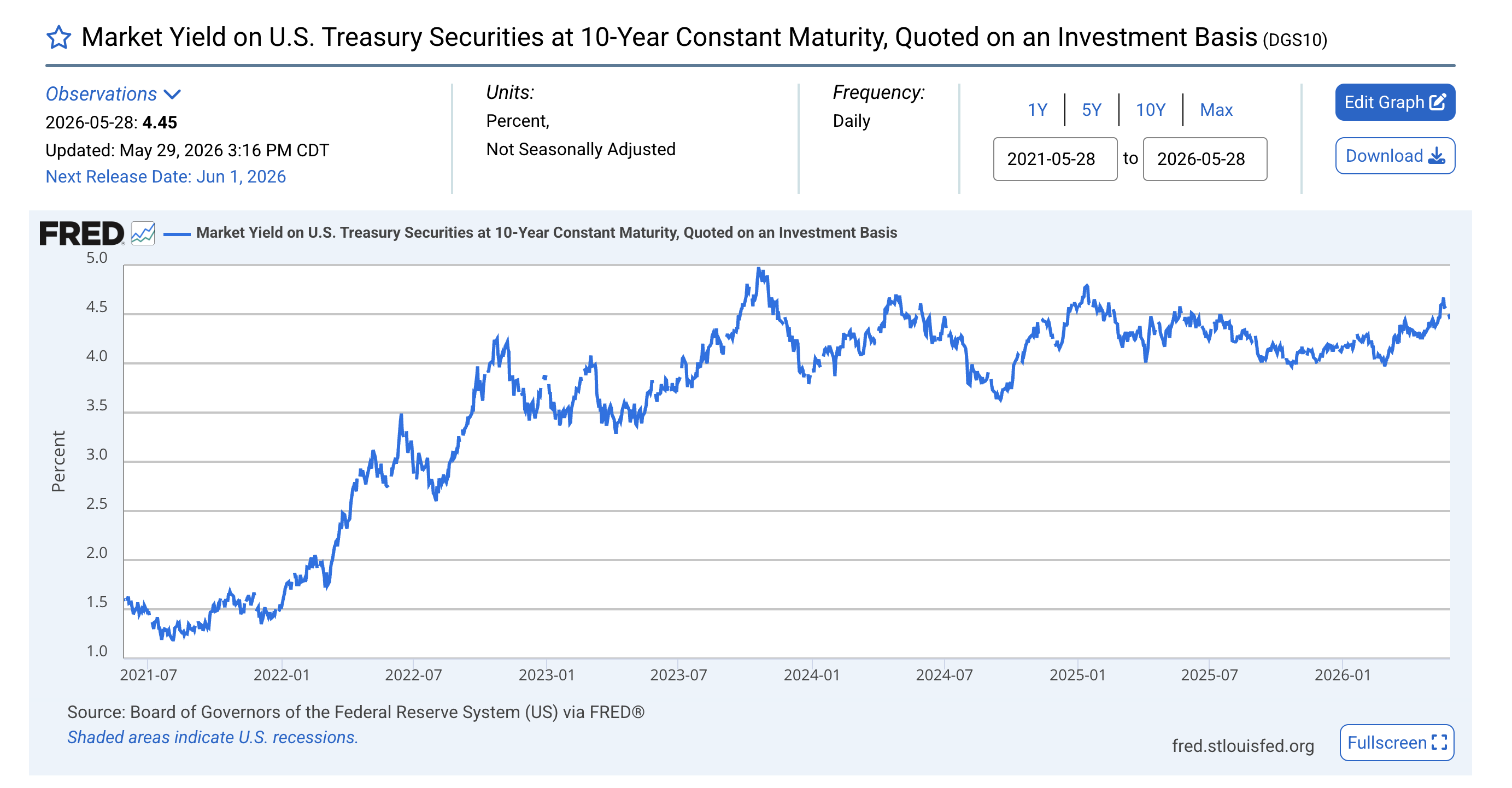

The Municipal Pressure Valve: By selling US Treasuries (USTs) into the open market, Warsh is deliberately suppressing bond prices and raising long-term yields. The 10-Year UST yield is hovering around 4.45%. This rise in long-term rates disproportionately impacts state and local governments (many in Democratic-leaning states like California, New York, and Illinois) that rely on cheap debt for infrastructure and services. Higher yields force these jurisdictions to either cut spending or raise taxes, creating political friction for the opposition party without the Fed officially "hiking" rates.

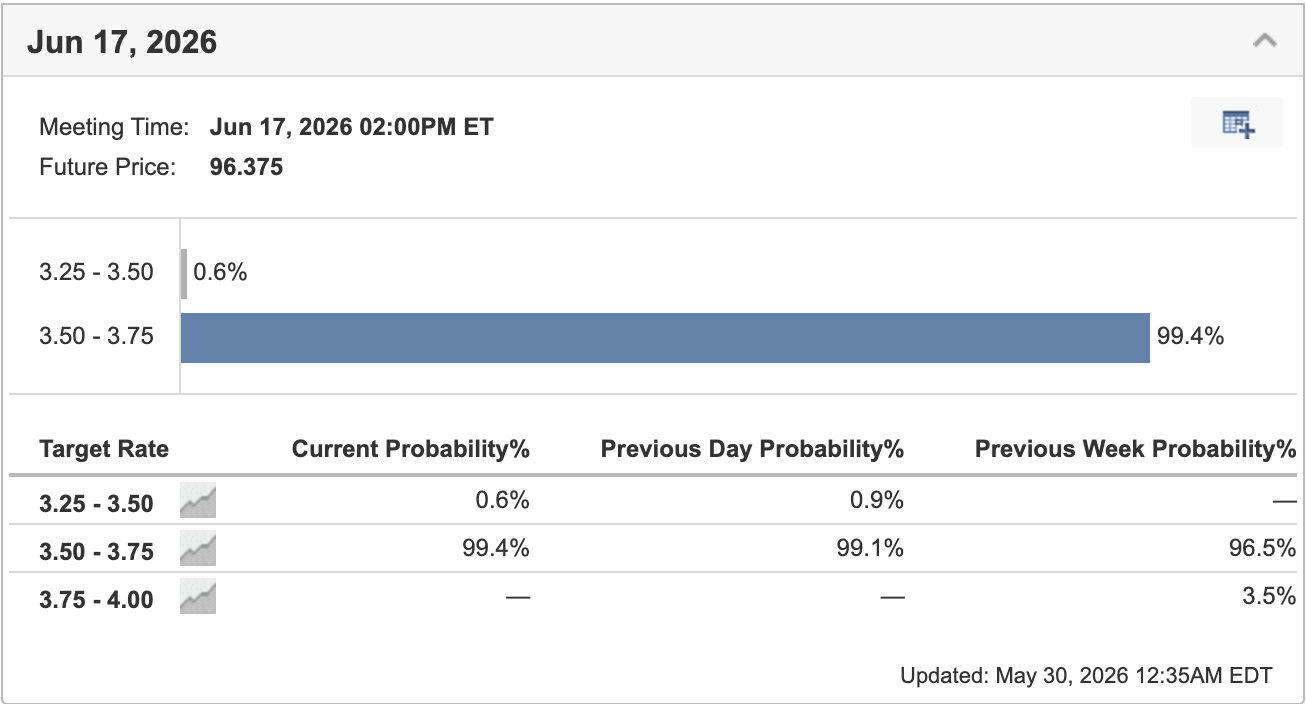

CME Group 30-Day Fed Fund futures prices data shows a 99.4% probability of the Fed holding rates unchanged at its June 16-17 meeting, reinforcing the view that Warsh’s primary lever is now balance sheet composition, not the funds rate.

This divergence creates a volatile environment for cross-asset flows:

USD/JPY & Carry Trade: The BOJ’s likely June hike contrasts with the Fed’s "higher for longer" yield curve via QT. This supports USD/JPY strength in the short term, but the narrowness of the BOJ vote (dependent on 2 swing members) introduces significant event risk. A surprise dovish hold from Masu or Koeda could trigger a sharp JPY rally as carry trades unwind.

Global Rates Correlation: HSBC forecasts that while the Fed holds, the ECB, BOE, and BOJ will all tighten in June-July 2026. This synchronized tightening outside the US reduces the relative attractiveness of non-USD assets, reinforcing USD demand despite political noise.

US Credit Spreads: Watch for wideningspreads in US High Yield and Municipal bonds. Warsh’s balance sheet reductionremoves a key buyer from the market, increasing supply pressure. IfDemocratic-led states face fiscal stress due to higher borrowing costs, expectpolitical rhetoric against Fed independence to intensify, potentiallyincreasing volatility in the front end of the yield curve.

- [TheJapanTimes]Japan’s inflation eases to four-year low, complicating BOJ hike, on May 22,2026

- [Axios]Battles to shrink the Federal Reserve's balance sheet begin, May 20, 2026

- [Investing.com]Fed Rate Monitor Tool, May 30, 2026

- [CNBC]Kevin Warsh gave his preferred way for measuring inflation. It could come backto bite him, on April 22, 2026

- [Reuters]US debt load could undercut Warsh's plan to shrink Fed balance sheet, on May15, 2026

- [Trading Economics]Japan Tokyo Core CPI YoY, on May 28, 2026

Focus: BOJPolicy Board Voting Dynamics, Fed Balance Sheet QT Impact, USD/JPY Carry TradeRisks

-min.jpg)