The Federal Reserve held its benchmark rate steady, but the internal debate over the path forward has intensified amid persistent inflation. Dallas Fed President Lorie Logan argued that further hikes may be necessary to confront sticky inflation, particularly in services and energy sectors. In contrast, New York Fed President John Williams stated that policy is "exactly in the right place," citing stabilizing labor data. The updated "dot plot" median rose to 3.8% for year-end 2026, signaling a higher cost of capital for long-duration assets despite the current pause.

Inflation dynamics remain geographically fragmented and elevated. The US Consumer Price Index (CPI) rose 4.2% year-over-year in May 2026, with energy prices surging 23.5% and shelter costs increasing 3.4%. The Personal Consumption Expenditures (PCE) price index, the Fed’s preferred gauge, increased 3.8% annually in April, with core PCE at 3.3%. Energy-intensive regions like Texas are experiencing overheating driven by oil price surges and AI infrastructure demand, fueling local wage growth. This regional unevenness complicates the Fed’s national mandate, necessitating a data-dependent approach that balances the risk of overtightening against the danger of entrenched inflation.

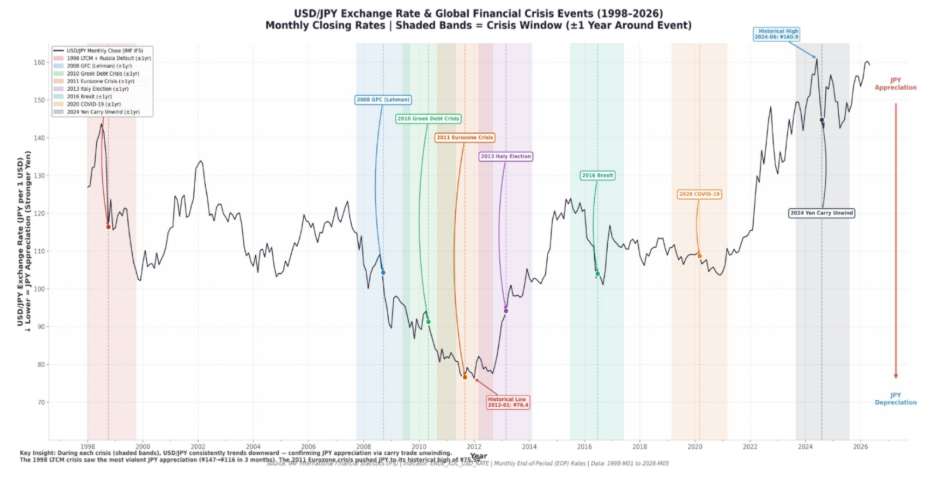

The Bank of Japan raised its policy rate to 1.0% on June 16, the highest level since 1995, marking a definitive step in its normalization cycle. Governor Kazuo Ueda’s absence due to hospitalization introduced communication uncertainty, with Deputy Governor Shinichi Uchida presiding over post-meeting briefings. Prime Minister Sanae Takaichi’s preference for accommodative policies adds a layer of political complexity to the trajectory of future rate moves. The BOJ’s underlying CPI inflation forecast remains above the 2% target, supporting the case for continued gradual tightening.

The narrowing US–Japan interest rate spread alters the mechanics of the yen carry trade. As the differential compresses, the incentive to borrow JPY to fund higher-yielding assets diminishes, reducing the relative payoff of leveraged positions. Historical data from the IMF International Financial Statistics and BIS Quarterly Review indicates that the yen tends to be appreciated during periods of global market stress as repatriation flows accelerate. This mechanical demand reinforces the yen’s role as a structural hedge against global deleveraging, independent of short-term yield differentials.

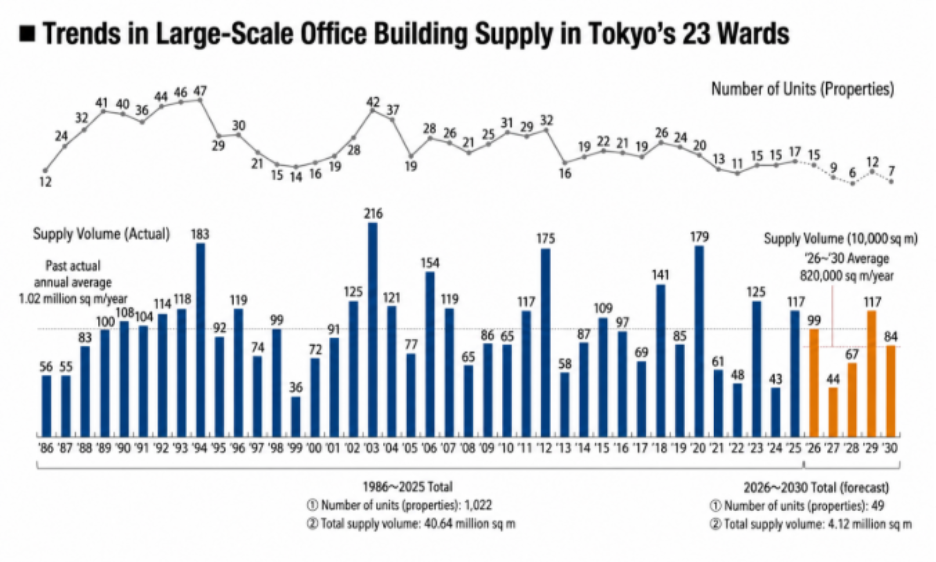

Tokyo's office market is genuinely tight. Mori Building reported net absorption of 1.64 million square meters in 2025—the third highest on record—with vacancy in major business districts down to 1.5%. New supply is thin, held back by construction of bottlenecks and a tilt toward office development.

That tightness lines up with Japan's broader push on AI. Efforts to keep the country from becoming an "AI colony" are pulling research and high-earning talent into Tokyo, which keeps demand for prime space stubbornly firm. The result is an "HQ premium" built on both physical scarcity and where strategic capital wants to be—the kind of setup that supports holding core-city assets for the long haul.

Taken together, these threads pointless to a single trade than to a way of reading the environment. A higher-for-longer rate backdrop tends to reward shorter-duration positioning, while assets priced on distant cash flows carry more sensitivity to where discount rates settle. The yen, for its part, has long behaved as a place capital retreats to when risk appetite turns—a role that has held up across cycles regardless of where yields sit. And in core markets like Tokyo, tight supply and concentrated demand have historically given prime assets a steadiness that doesn't depend on the near-term cycle.

The common thread is location and structure over timing—where capital sits, and how durably, rather than what moves next.

Sources

-min.jpg)