The traditional diversification model, negative correlation across equities, bonds, and gold, is under strain. The catalyst is concrete: the US–Iran conflict has passed its 100-day mark with the Strait of Hormuz still closed, keeping oil elevated and feeding the inflation that pressures bonds. Equities have bifurcated rather than uniformly declined: US benchmarks sit at record highs led by a narrow set of AI beneficiaries, while energy-import-dependent markets struggle and gold shows elevated correlation with risk assets during liquidation episodes. Resilient indices and stressed funding conditions can coexist, deleveraging pressure surfaces first in bonds, gold, and FX, not the equity tape.

In this context, the yen functions as a structurally driven defensive asset, not because of Japan's growth prospects, but because of the carry trade. Low Japanese rates have long funded high-yielding assets globally; when volatility spikes, those positions must close, and closing a JPY-funded carry trade requires buying back yen, non-discretionary demand independent of Japan's economy. The point is not that the yen "will rise," but that an identifiable mechanism links deleveraging to yen demand, one to build into scenario planning.

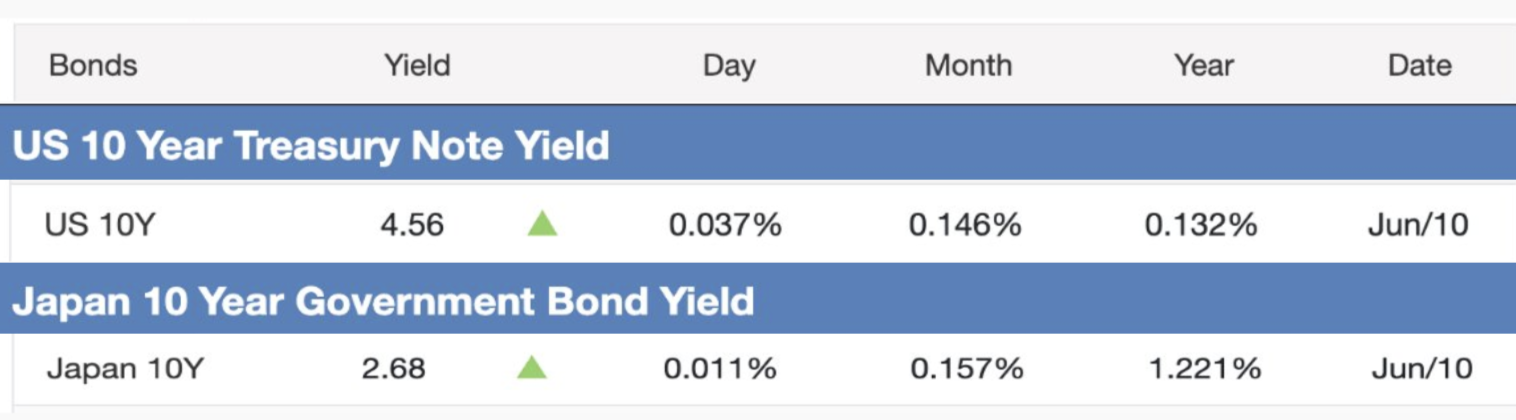

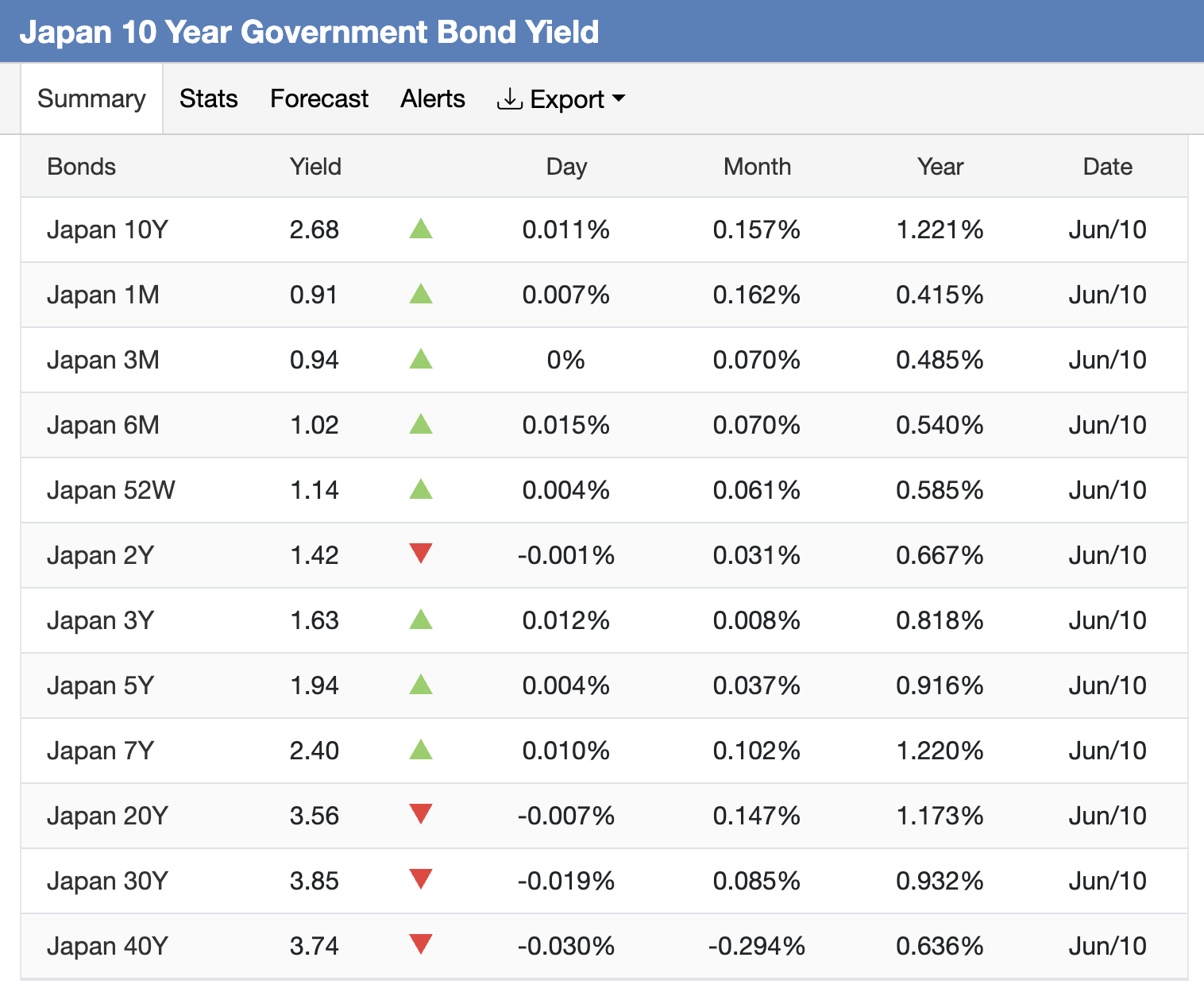

The foundational variable is the yield spread: with the US 10-year near 4.54% and Japan's at 2.71%, a differential of roughly 180 basis points favors dollar assets and capital chases the higher carry for as long as the spread stays wide.

One scheduled source of variance: the November 2026 US electoral calendar adds policy uncertainty to rate and fiscal expectations.

Positioning around this anchor is split institutional flows align with the differential, visible in weekly futures data from the US Commodity Futures Trading Commission, while much of the retail base is positioned for a yen recovery yet to materialize. Positioning this one-sided amplifies moves in either direction; a narrowing differential or official intervention could force a rapid unwind.

“We bring forward our long-held rate hike call from July to June and now expect a 25bp increase to 1.00% at the upcoming meeting. The key focus will be the BOJ’s updated assessment of the neutral rate, as well as any forward guidance on the potential for additional hikes in the second half of the year. Given current inflation readings, trimmed mean CPI at 1.5%, core CPI (excluding fresh food) at 1.4%, and core CPI (excluding fresh food and energy) at 2.0%—we estimate the neutral rate should be at least around 1.5%. On the fiscal side, recent government measures may help temper but are unlikely to fully alleviate investor concerns about fiscal sustainability.” said Ma Tieying, CFA, Senior Economist, Japan, South Korea, & Taiwan, DBS.

The takeaway is not directional: the spread defines the prevailing flow; crowding and the intervention zone define where volatility concentrates.

The Bank of Japan cannot hike aggressively without inflating government debt-servicing costs, nor lean on tax increases against stagnant demographics. Its available response is curve management plus expanded issuance: hold the short end steady and concentrate new supply further out the curve, potentially via new ultra-long categories (50- and 60-year JGBs), a discussed option rather than announced policy. The curve already shows it: the 2-year sits near 1.42% while the 20- and 30-year have risen to roughly 3.62% and 3.93%.

Incremental normalization is nonetheless in motion: ahead of the June 15–16 meeting, Governor Ueda’s signaling pushed market-implied odds of a 25-basis-point hike to roughly 85%, which would lift the policy rate to its highest since 1995, though analysts frame it as a single step rather than an accelerated cycle. The variable to monitor is the short end, benchmark rates such as Japanese Yen: a 25-basis-point step adjusts, but does not dismantle, the carry trade's funding structure. A credible shift to a faster hiking path would be the genuine regime of change.

AI is moving from speculative experimentation to industrial deployment, measurably so: a May 2026 Reuters survey found one-third of Japanese companies using or considering AI-powered robots, which the government sees as key to its chronic labor shortage.

Japan runs a dual-engine model:

while

As AI firms shortlist Asian bases—Singapore, Japan, India, Japan's financial depth strengthens Tokyo's claim as the sector's institutional anchor. Critically, the HQ function is a talent function: talent flows, not factory locations, determine where office and residential demand accumulate.

Sources

-min.jpg)